CEICData.com © 2018 Copyright All Rights Reserved

The Thai baht was one of Asia's best-performing currencies in 2025, appreciating almost 10% to a multi-year high against the US dollar despite disappointing tourist numbers, political instability and US tariffs on ASEAN exporters.

The strong currency has been partly linked to the record rally for gold. The precious metal is a favored store of wealth for Thai households, and the nation plays a disproportionate role in global gold trading.

However, we can also link the baht's gains to balance-sheet flows. Whether due to business success or a defensive stance, Thai firms have been repatriating capital from overseas -- and it's become enough of an issue for the currency that the central bank has proposed raising the limit on foreign income that companies can keep offshore.

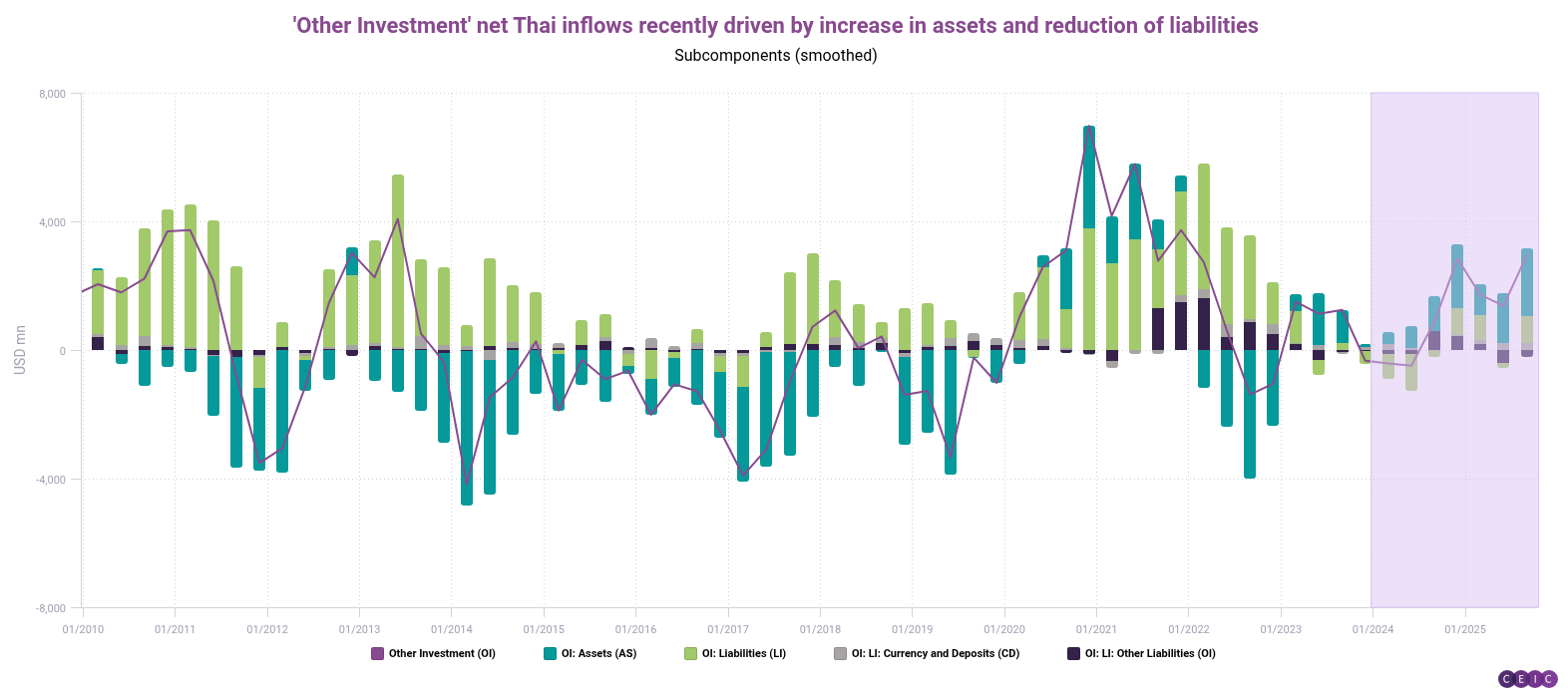

We can identify this phenomenon (and isolate it from other common currency drivers) by charting the correlation between the exchange rate and "other investment" in the Thai central bank's balance-of-payments figures. "Other investment" is a catch-all category that records cross-border financial positions and transactions not classified as direct investment, portfolio investment, financial derivatives, employee stock options, or reserve assets.*

As our first chart shows, the correlation got much stronger after the pandemic, and "other investment" has been ticking higher for a year and a half, resulting in steady one-way foreign-exchange inflows.

Compare this correlation to two other common currency drivers linked to external speculative flows. Our second and third charts consider foreign inflows into Thai equities and yield differentials between Thai and US government securities. These have had their moments of correlation, but not lately.

.png?width=774&height=805&name=Bahts%20correlation%20with%20equity%20market%20inflows%20weaker%20than%20it%20was%20pre-2020%20(1).png)

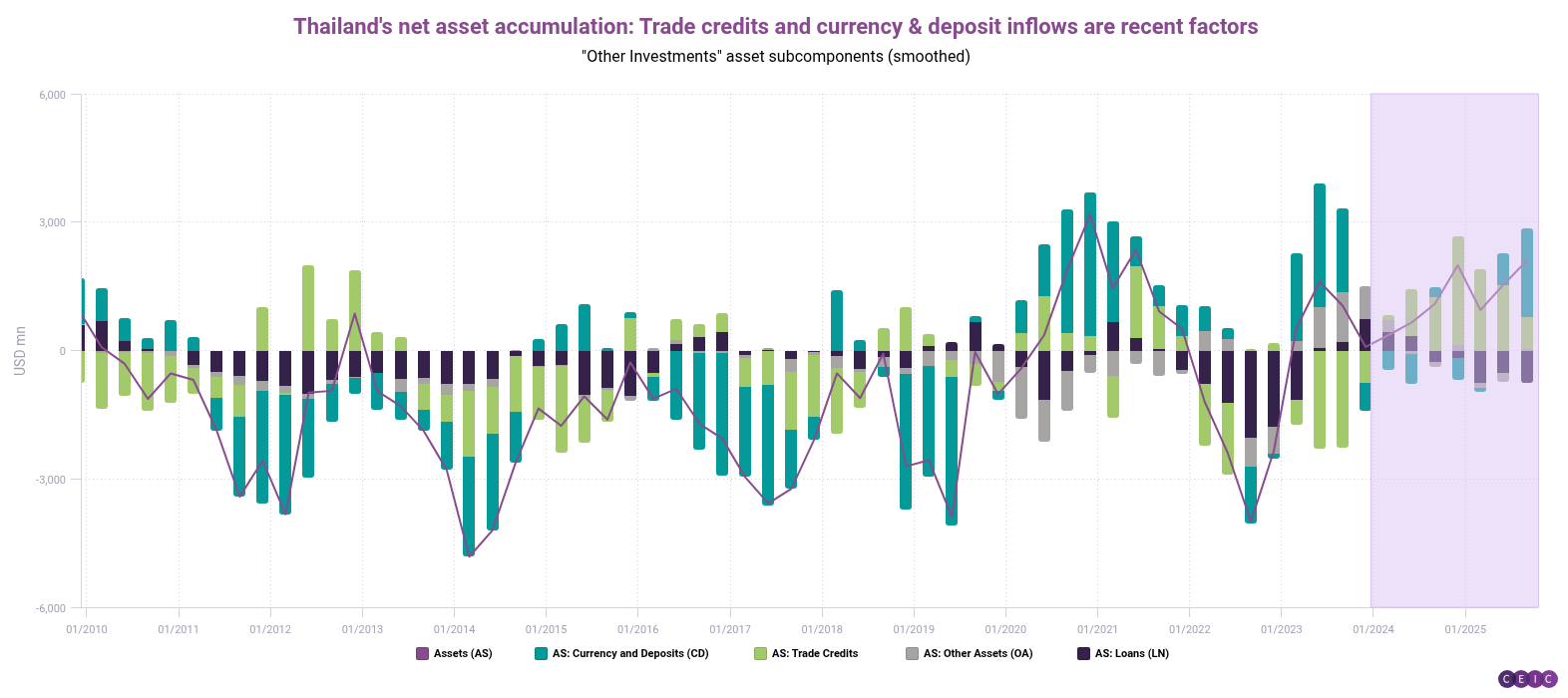

Our subsequent charts break down more flows tracked by the Thai central bank and their subcomponents, including details of "other investments."*

.png?width=1572&height=700&name=Thailands%20overall%20balance%20has%20been%20positive%20since%202024%20supporting%20baht%20appreciation%20(1).png)

*More on "other investment": It mainly covers bank- and firm-level balance-sheet items, including currency and deposits, loans, trade credit, insurance and pension reserves, other equity, accounts receivable/payable, and SDR allocations. In essence, it captures operational financing, liquidity management, and credit relationships rather than ownership or market-traded securities.

Thai banks and corporates with a preference for domestic funding or greater risk aversion given US trade policies may be using their extra cash to repay foreign-currency liabilities and reduce offshore funding, which would show up in this category; foreign investors, attempting to hedge against dollar weakness, may also play a part in these flows.

If you are a CEIC user, access the story here.

If you are not a CEIC client, explore how we can assist you in generating alpha by registering for a trial of our product: https://hubs.la/Q02f5lQh0