The resilience of emerging markets M&A in the face of such an overpowering mix of local and global challenges throughout 2018 has been admirable and full of promise, to say the least. In addition to economic disruptors such as the seemingly endless Brexit squabbles and the tit-for-tat US-China trade conflict, elections in key developing economies (e.g. Brazil, Mexico, and Russia) and tumbling currencies in Latin America and Europe resulted in additional market uncertainty.

However, cheap funding and modest organic growth created enough incentives for unflinching deal-makers and as a result there were no dramatic falls in deal activity in 2018, save from Argentina, whose peso lost nearly half its value this year, leaving the economy in shambles.

The trade tensions between the world’s two largest economies provoked some investors to reduce their holdings in riskier assets, i.e. assets in emerging markets. But it sure isn’t unlikely that many countries will stand to benefit from this rivalry as Chinese private investors won’t cease to in-vest overseas despite tightened government regulation on outbound capital. What is more, manufacturing industries in Asia, Latin America, and elsewhere could serve as alternative import destinations for the US, and developing nations as a whole could be forced by circumstances to introduce reforms that could lead to economic growth in the long term.

Going forward, all these global challenges could strengthen those emerging economies willing to adapt, thus further boosting their M&A attractiveness.

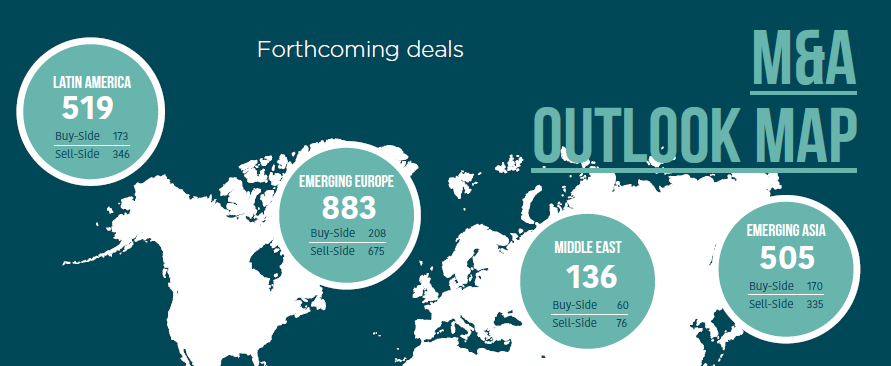

Latin America

After a string of pricey acquisitions in the first half of 2018, deal-makers became more prudent. Share offerings were also subdued. In Brazil, after a spectacular 2017, the number of IPOs and SPOs fell from 23 to just 6 and a single company, fintech PagSeguro, ac-counted for more than half of the USD 6.5bn raised. On the bright side, Chile saw its largest-ever IPO of MallPlaza, and the Brazilian bourse saw its first fin tech, Banco Inter.

If campaign promises about deregulation, privatisation, and reforms are kept by Brazil’s right-wing president-elect Jair Bolsonaro and right-wing Colombian president Ivan Duque, much of the market volatility might sink. In Mexico, with new president AMLO, privatisation is likely to be suspended. Although his market friendliness was questioned after he scrapped a mega airport project, chances are that he will allow oil and gas giant Pemex to continue farming out projects to boost output.

Brazil will retain its dominant role in the region. Rumour has it the country will auction off valuable crude oil assets, while Petrobras, whose privatisation is not a priority for Bolsonaro is said to seek another USD 20bn from asset sales. Also, at least two dozen Brazilian firms are weighing share sales in the imminent future. Argentina, whose peso has been the worst-performing emerging market currency in 2018, will need some time before it restores market confidence and an uptick in M&A seems unlikely.

More deals can be expected in the mining sector, especially in the coveted lithium industry in Chile and Argentina. M&A activity in the medical cannabis industry of Colombia, Argentina, Chile, Peru, and Uruguay is also possible and there have already been several in-bound deals.

Emerging Europe

“They are looking into nearly everything,” sources in Turkey told media regarding the visits of Chinese investors eyeing Turkish as-sets. The lira’s 2018 sell-off and the US dollar/ lira exchange rate have created favourable conditions for foreign buyers while leaving local businesses struggling to repay debts. Conglomerates have been selling their prized assets and some companies may be forced to consider deleveraging options. Indeed, the largest deal in the country in 2018 was the debt restructuring of Turk Telekom.

The biggest economy in the region, Russia, is undergoing its own challenges and the impact of US and EU sanctions has spread to M&A. Foreign investors and significant transactions are exceptions in any industry except oil & gas and there has been a wave of company delistings from the Moscow Exchange. Deals are mostly between domestic players and for now, we foresee no significant M&A activity in 2019, as Moscow does not plan major privatisations soon.

But it was not all doom and gloom in Eastern Europe. M&A deal flow in Poland was stable and even improved during some of the quarters – some local businesses were very acquisitive and consolidation is expected in banking, debt collection, real estate, and telecoms, although two deals for the same Polish cable operator collapsed in 2018. In Europe’s southern end, Romania demonstrated a steady deal flow and could remain an attractive destination for both PE and strategic buyers.

Africa and Middle East

In Africa, investments show no sign of slowing down. In pursuit of minerals for the electric vehicle industry, Chinese miners are snapping up stakes in promising copper and cobalt deposits. Mali-focused Canadian miner Randgold is merging with Barrick, creating the world’s top gold miner. In addition, several Asian countries including South Korea, Singapore, and Malaysia are looking to tap into the vast opportunities of the continent. The energy sector in East and Central Africa also holds strong potential. In the Middle East, investors’ sweetheart Saudi Arabia was splurging on assets through its Public Investment Fund as it looked for alternatives to oil. Then suddenly, it postponed indefinitely the world’s potentially largest IPO – that of oil giant Aramco. Weeks later, the death of Saudi journalist Jamal Khashoggi gravely undermined Riyadh’s image and it is anybody’s guess whether Saudi Arabia will suffer from an isolation akin to Qatar’s following the Gulf crisis in 2017. Both Saudi Arabia and the UAE are planning privatisations of state- and semi-state-owned firms. Iran, too, has earmarked for privatisation 631 companies by the end of March 2019, Oman has a healthy IPO pipeline of mainly utilities, and Bahrain has launched a USD 100mn venture capital fund.

Emerging Asia

China’s outbound deals were hit by fears of a full-blown trade war with the US and several blocked China-led acquisitions of US targets. The gov-ernment curb on capital outflow got in the way of traditionally acquisitive conglomerates such as HNA, Fosun, and Anbang. All three are expected to generate deal activity but this time on the sell side.

Other emerging Asian markets, however, may benefit from trade tensions. Vietnam has become an attractive deal destination with its high economic growth, young population, and ongoing capital market reforms. Sectors with M&A potential include real estate, consumer goods, health-care, banking and fin tech, renewable energy, and infrastructure. In India, 2018 saw the largest ever inbound strategic acquisition – the USD 16bn buy of Flipkart by US Walmart. This could be the beginning of a stellar M&A season if the H1 2019 general election goes smoothly. The overhaul of the insolvency and liquidation procedures in the country could lead to more M&A deals and there is also an impressive IPO pipeline.

The Hong Kong stock exchange, which altered listing rules to allow pre revenue biotech firms to list, is on track to end 2018 as the top listing venue globally. The trend is set to continue as a total of 250 companies are in the pipeline for 2019.