CEICData.com © 2018 Copyright All Rights Reserved

Christmas 2025 saw a weaker seasonal spending impulse across advanced economies. While households continued to spend through the year, the traditional end-of-year uplift (adjusted for inflation) narrowed materially, particularly for discretionary items such as electronics, clothing and sporting goods. This matters because household consumption has long been the most stable contributor to growth for advanced economies.

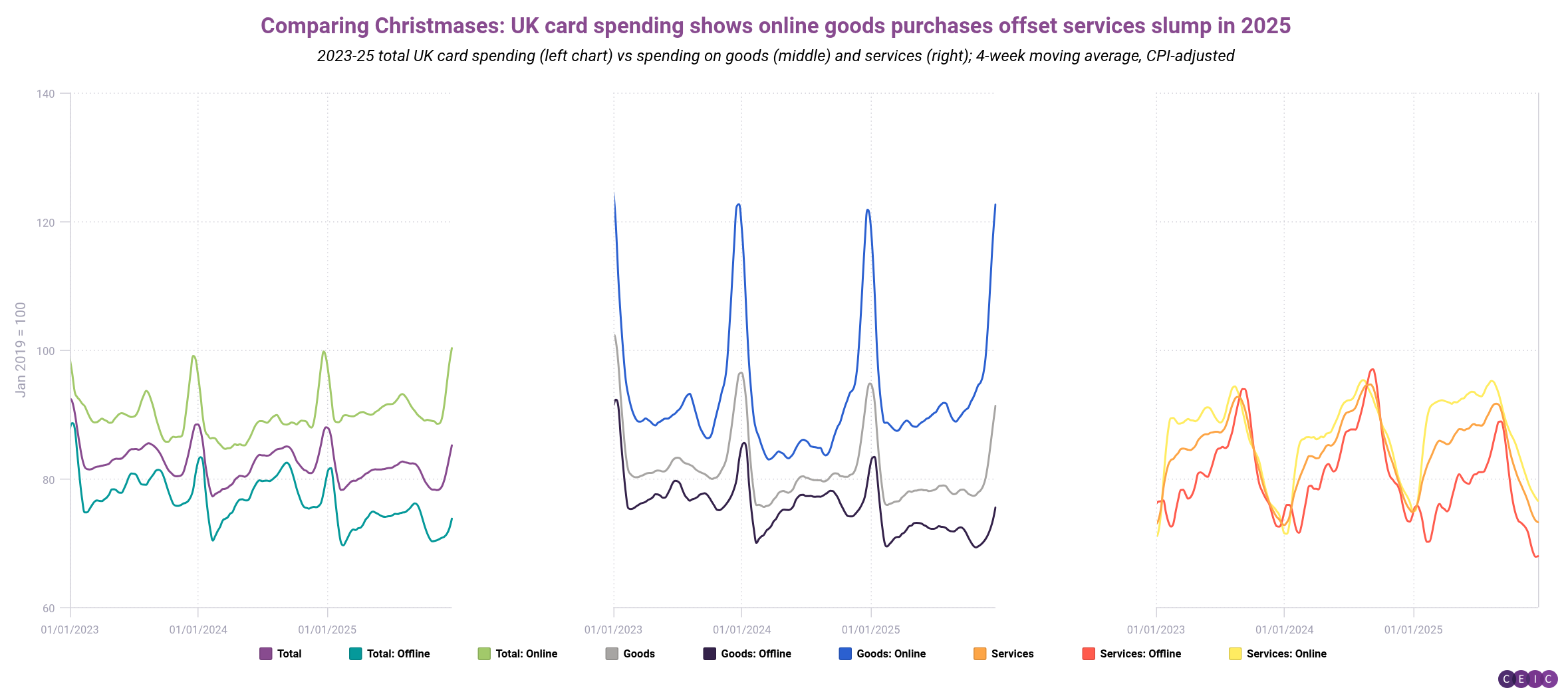

Our first chart focuses on the UK, tapping the power of high-frequency datasets on payment-card spending. The Christmas premium — the gap between baseline spending and year-end peaks — has become more uneven. What uplift remains is largely concentrated in goods bought online; for bricks-and-mortar retail outlets, goods and services purchases displayed little meaningful seasonal acceleration. Christmas is functioning less as a positive demand shock and more as a redistribution of spending across channels and timing.

The US data in the second chart sends a warning signal. Real, CPI-adjusted card spending on Christmas-related goods remained below 2021–2023 trends across most major discretionary categories, though it slightly surpassed 2024 levels. Electronics and household goods, typically the backbone of holiday spending, underperformed most visibly. Clothing and accessories also failed to generate the same late-season surge observed in previous years. This weakness occurred despite positive real wage growth, suggesting deliberate restraint in discretionary spending rather than income-related stress.

The UK experience is consistent but nuanced. Aggregate real card spending through 2025 was higher than in most previous years, reflecting solid underlying consumption dynamics. However, the Christmas period itself looks unremarkable by recent standards. This suggests households are smoothing consumption over the year rather than concentrating discretionary purchases in December.

In Germany, CPI-adjusted card spending on Christmas goods in 2025 remained clearly below the levels seen over the previous five years. This pattern aligns with a more cautious household sector shaped by weaker income dynamics and elevated precautionary saving.

The consistency across all three nations points to a broader slowdown in discretionary demand in the last quarter of 2025; the macro implications are uncomfortable. If labour markets soften or real wage gains fade in 2026, the absence of a strong seasonal buffer would amplify downside risks.

If you are a CEIC user, access the story here.

If you are not a CEIC client, explore how we can assist you in generating alpha by registering for a trial of our product: https://hubs.la/Q02f5lQh0