CEICData.com © 2018 Copyright All Rights Reserved

The eurozone's economy expanded by 1.3% in the fourth quarter of last year, roughly matching its 3Q pace and extending a modest recovery. However, breaking down the factors influencing GDP in previous quarters highlights sustained export weakness driven by trade uncertainties. External demand has struggled to gain traction amid strong competitive pressure from Chinese exports and Donald Trump's tariffs on shipments to the US.

Net exports declined for five consecutive quarters through Q3 of 2025. That's offset relatively robust investment growth (driven by defense spending and improved financial conditions) and a continued contribution from household consumption.

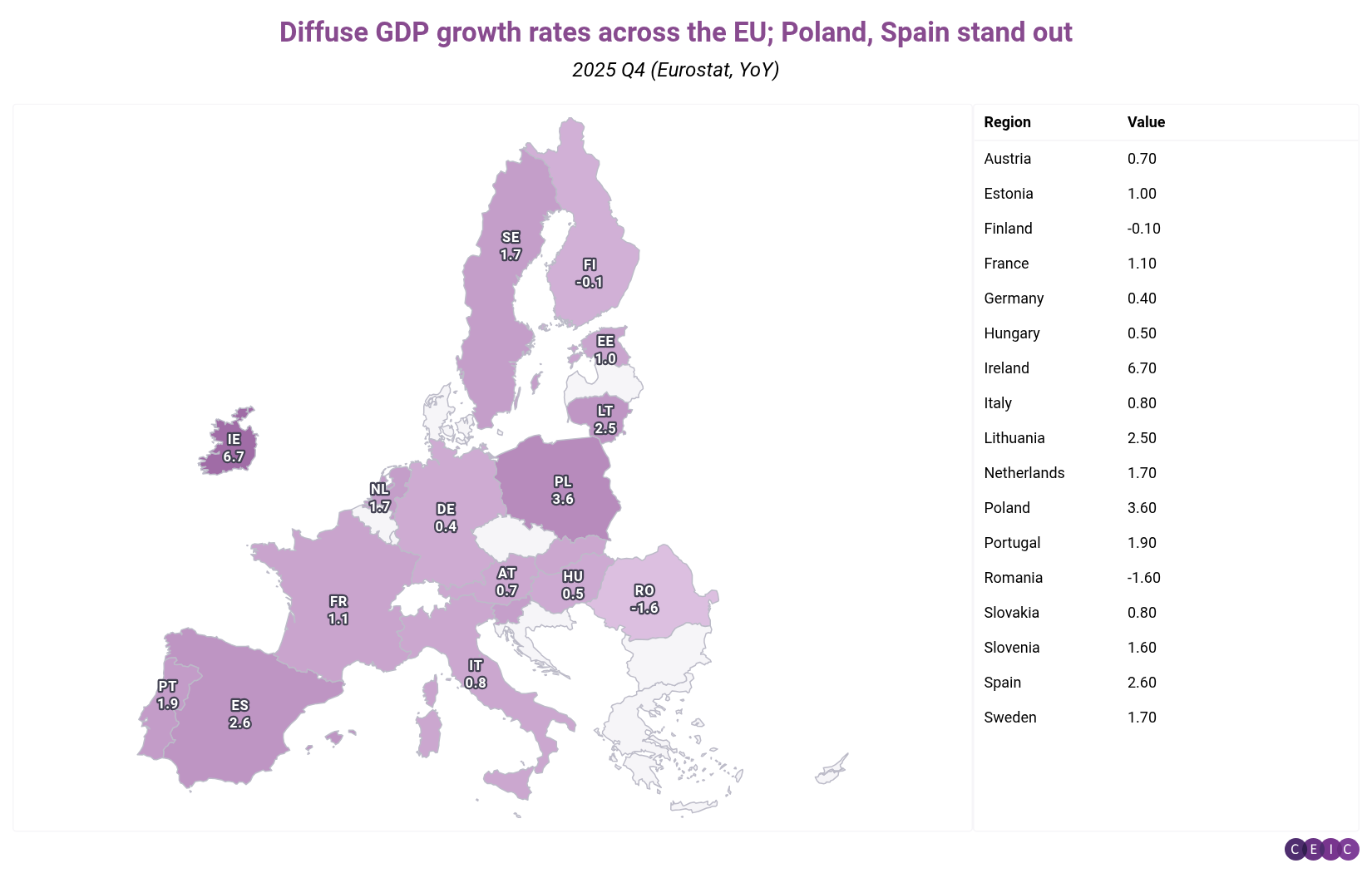

This aggregate picture masks significant cross‑country divergence, as shown in our second and third charts. Growth outcomes range from near‑stagnation in core industrial nations to strong expansion in more service‑ or tourism-driven economies. Germany, Austria and Finland posted weak or flat performance; Ireland, Poland, Portugal and Spain have seen robust growth.

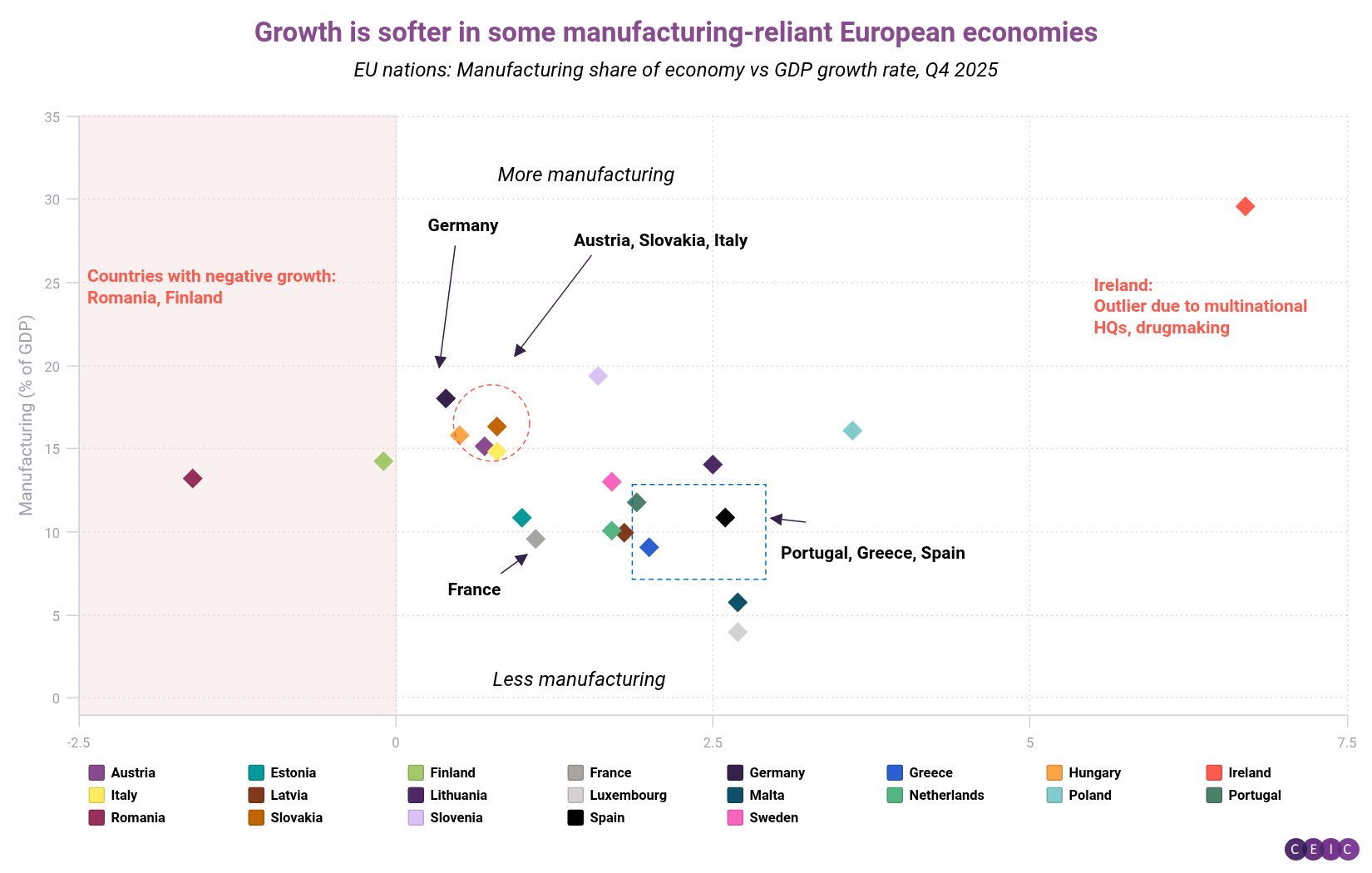

Our third chart compares countries' growth rates to their dependence on manufacturing. Germany, Slovakia and Austria were clustered at the lower side of the growth distribution in Q4. Portugal, Greece and Spain form another cluster, with stronger growth and less manufacturing in the GDP mix versus services. Ireland remains the most notable outlier amid high dependence on pharma exports and GDP figures boosted (and distorted) by multinationals' head offices and tax treatments.

Turning back to the Eurozone as a whole, an analysis of S&P's purchasing managers' index (PMI) shows how services are supporting growth. The services sector has consistently remained above the expansion threshold for most of 2024–25; manufacturing PMI remained in contractionary territory for much of the past two years, with only tentative stabilization toward the end of 2025. Construction activity continues to lag despite support from the EU's Recovery and Resilience Facility.

CEIC's proprietary nowcasts (based on high-frequency data) highlight a striking divergence between the EU's two biggest economies so far in 2026. Germany's weak recovery appears to have come to a halt as industrial output stumbles. By contrast, France's economy is picking up, supported by a surge in the PMI output index.

What are the wider implications of these trends? the European Central Bank has held rates steady since last June. While most of the institution's central bankers show little inclination to cut further, a recent blog posted by the ECB argued that lower borrowing costs could reduce the drag on growth caused by US tariffs.

If you are a CEIC user, access the story here.

If you are not a CEIC client, explore how we can assist you in generating alpha by registering for a trial of our product: https://hubs.la/Q02f5lQh0