CEICData.com © 2018 Copyright All Rights Reserved

.png?width=1140&height=390&name=Flows%20to%20US%20equity%20funds%20slow%20to%20a%20trickle%20amid%20weak%20dollar%20tariff%20concerns%20(4).png)

As Donald Trump's post-tariff landscape for international trade takes shape, global fund flows are diverging. After a series of trade deals reached with Japan, the European Union and other markets, inflows have resumed in most of the world -- but not the US.

According to exclusive fund-flow data from our partners at EPFR, net inflows to US-based equity funds began waning as soon as the US president took office and stepped up his trade rhetoric. Inflows contracted further after the "Liberation day" announcement of tariffs on almost every country in the world. But as the Trump administration reached a patchwork of deals this summer, inflows fell even further, and are barely in positive territory.

As our chart shows, this trend coincided with a weak greenback (as measured by the Dollar Index). International investors may be concerned that a falling USD will erode the value of their investments; in turn, as those investors deploy capital elsewhere, one of the supports for the currency is removed.

The current situation is in marked contrast to the optimism that followed Trump's election win last year. Despite his repeated campaign pledges to disrupt the global trading system, money poured into US equity funds (and their bond counterparts) amid expectations for pro-business fiscal and deregulatory policies, helping lift the dollar; investors assumed tariff implementation would prove milder than Trump's rhetoric suggested.

Today, job figures suggest the US economy is weakening. Meanwhile, sticky consumer prices limit the Federal Reserve's scope to cut rates: our second chart demonstrates how tariffs are being priced in to inflation expectations.

Our subsequent charts show how flows have been redirected to Europe, Asia and bond funds.

US bond funds are notable because, like the dollar, the usual safe-haven relationship broke down after Liberation Day. As assumptions about US geopolitical, economic and trade policies were upended, growth expectations were downgraded but investors did not deploy capital to US fixed income. As more clarity has emerged, the traditional relationship appears to have returned; with GDP forecasts for 2026 still depressed (according to surveys from FocusEconomics), bond-fund inflows resumed.

European funds, meanwhile, appear to have benefited from a diversification push. These fund inflows have in turn supported the euro.

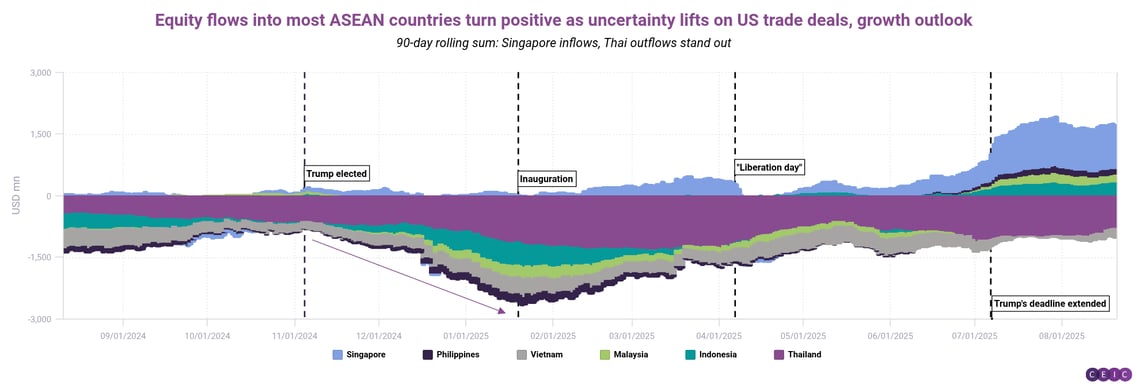

Rotation into non-US assets has also boosted ASEAN inflows, which shifted once trade agreements began to be reached.

Click here to read about Trump's *Liberation Day* tariffs and analyzing USD turmoil and recovery of haven status post-Liberation Day.

If you are a CEIC user, access the story here.

If you are not a CEIC client, explore how we can assist you in generating alpha by registering for a trial of our product: https://hubs.la/Q02f5lQh0